Commercial Credit Report: A Complete Guide for Risk-Free Trade

A commercial credit report helps you trade more safely by showing who the counterparty really is, how stable they are, and how much trade credit exposure makes sense. Used well, it turns credit information into practical terms: limits, payment days, safeguards, and review frequency.

Definition: What is a commercial credit report?

A commercial credit report is a decision-focused credit report that combines verified identity details with indicators of credit risk. By supporting repeatable risk assessment it allows you to approve (or restructure) deals with greater confidence.

1) Risk-free trade doesn’t mean “no risk”—it means “controlled exposure”

In B2B, risk often comes from two gaps:

- You don’t fully know the legal entity you’re contracting with.

- You extend more credit than the counterparty can realistically carry.

A commercial credit report helps close both gaps—especially before first shipment, limit increases, or long payment terms.

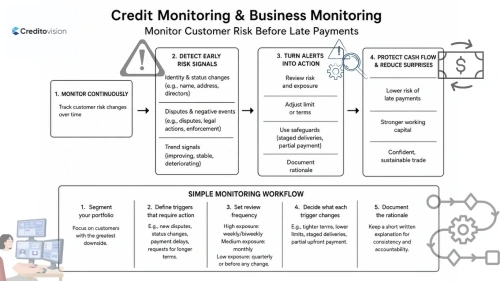

2) What a good commercial credit report actually contains (and how to read it)

A commercial information report can include the sections below. The key is how you interpret them.

A) Identity and legal structure (the “contract safety” layer)

- Legal name, registration identifiers, status (active/inactive)

- Legal form and address footprint

- Ownership/management and recent changes

How to use it: If the report suggests ambiguity (multiple similar entities, frequent changes, mismatched details), treat it as a risk signal. Many costly disputes start with “We contracted with the wrong entity.”

B) Payment behavior indicators (the “willingness/discipline” layer)

- Patterns of late payments vs. isolated delays

- Signs of collection pressure (where available)

- Notes that suggest strained supplier relationships

How to use it: Don’t overreact to one delay. Look for repetition and escalation. Patterns matter more than anecdotes.

C) Negative events and legal issues (the “hard constraint” layer)

- Disputes, enforcement actions, insolvency steps (where available)

How to use it: When active negative events appear, lowering the limit is not enough. You should also tighten the structure: shorter terms, staged shipments, partial upfront payment, or secured methods.

D) Risk indicators and recommendations (the “decision layer”)

Many reports include a risk score plus recommendation-style guidance.

How to use it:

- Score = how cautious you should be

- Evidence = why the score exists

- Terms = what you do next (limit/terms/safeguards)

A score is most valuable when you translate it into consistent actions.

3) Turning the report into terms: a practical decision matrix

Instead of debating each case from scratch, use a simple matrix that converts credit risk into conditions.

Decision matrix (easy to apply)

- Low risk + stable identity + no negatives

→ Standard terms (e.g., 30 days), normal limit, routine review - Medium risk OR limited data

→ Smaller limit, shorter terms (15–30 days), staged delivery, manual approval for increases - Higher risk OR active negative events

→ Avoid open terms; require safeguards (deposit/advance payment/LC), keep exposure small, re-check frequently

This is everyday risk management: align exposure with evidence.

4) Common mistakes that create avoidable losses

These are frequent “trade losses” even in otherwise good businesses:

- Confusing brand vs. legal entity: the logo is not the contracting party.

- Approving terms based on order size: a big order doesn’t mean a stable payer.

- Ignoring “recent change” signals: sudden management/ownership changes often matter more than old history.

- Using the report once and never revisiting it: conditions change; your exposure grows.

5) How to use commercial credit reports inside a real workflow

To avoid the “report sits in a folder” problem, embed it into your process.

A practical workflow:

- Pre-check (before quote/first shipment): run a credit check and verify identity fields.

- Set terms (before contract): decide limit + payment days + safeguards.

- Release control (before shipping): staged shipments if risk is not low.

- Review triggers: re-check before limit increases, after disputes, or when payments slip.

- Documentation: store the decision rationale (simple but consistent).

Reports may be compiled by credit reporting agencies, but the outcome depends on how consistently you apply your rules.

Practical Checklist: Using a commercial credit report in 6 steps

- Confirm the legal entity (name + identifiers + status) matches the contracting party.

- Check for recent structural changes (ownership, directors, address).

- Scan negative/legal events (treat active items as constraints).

- Review payment behavior for patterns.

- Translate risk into terms (limit, payment days, safeguards).

- Re-run the review before you increase exposure.

FAQ

What if the report has limited data?

Treat limited data as uncertainty, not as safety. Start with smaller exposure, shorter terms, and staged shipments until payment performance is proven.

Is “risk-free trade” realistic?

Not completely—but “controlled risk trade” is. A commercial credit report helps you structure deals so one bad payer doesn’t become a major loss.

Conclusion

A commercial credit report becomes powerful when you use it as a decision tool—not just a document. Read it in layers (identity, behavior, negatives, risk score) and convert findings into clear trade credit terms. That’s how you reduce credit risk without slowing down growth. To explore how reliable commercial credit reporting can support safer trade decisions, visit Creditovision. https://portal.creditovision.com/login