Credit Monitoring & Business Monitoring: How to Monitor Customer Risk Before Late Payments

Credit monitoring helps businesses identify changes in customer risk before invoices become overdue. Instead of relying on a single report at the start of a relationship, business monitoring keeps exposure aligned with what is happening now. That matters when payment terms are extended, balances increase quietly, and warning signs appear before late payments become visible in your ledger.

What does credit monitoring mean in B2B?

In B2B trade, credit monitoring is an ongoing process used to track meaningful changes in a customer’s profile over time. It supports earlier decisions on limits, payment terms, and safeguards before risk becomes costly. In practice, it often works alongside customer monitoring, combining alerts and periodic reviews to support a more consistent customer risk assessment.

Why one-time checks are not enough

A one-time customer risk check may be useful when a relationship begins, but it does not protect you if the customer’s situation changes later.

Risk can shift quickly because of:

- ownership or management changes

- new disputes or legal events

- sudden growth that puts pressure on cash flow

- sector conditions that weaken payment behavior

This is why many teams use customer risk monitoring for accounts where exposure can grow over time. A customer that looked acceptable three months ago may no longer deserve the same limit or terms today.

What to monitor and what it tells you

A practical monitoring process should focus on decision triggers, not noise. The goal is not to collect more updates. It is to detect the changes that should influence your next credit decision.

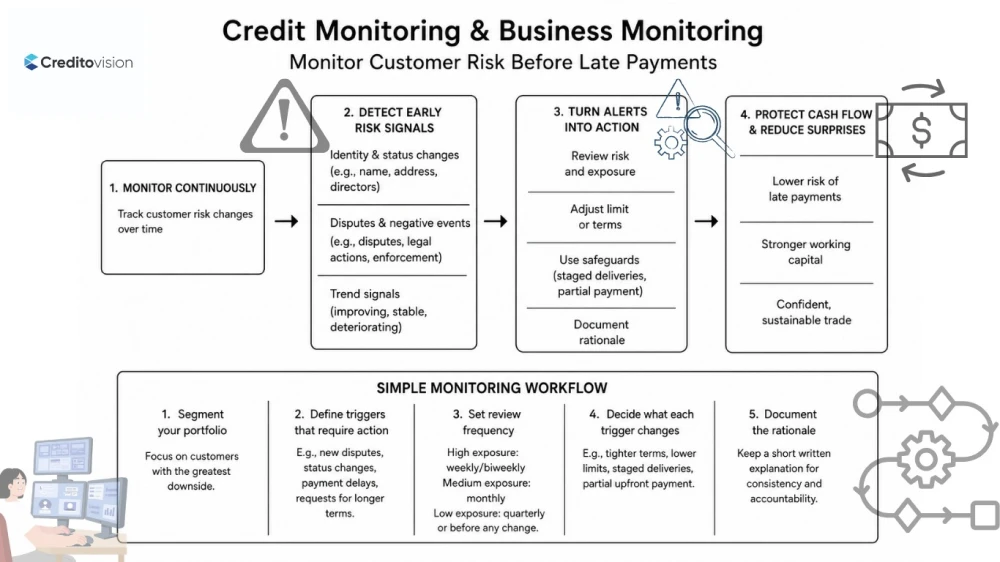

1) Identity and status changes

If legal entity details change, such as name, status, or address, confirm that you are still trading with the correct party. This is where a company information report becomes especially useful, particularly when the contracting entity must be precise.

2) Negative events and disputes

New disputes, enforcement steps, or other negative signals are rarely harmless. Even when a customer is still paying on time, these developments can indicate growing pressure that may affect future payment performance.

3) Trend signals

The most useful monitoring is directional. It helps you understand whether conditions are improving, stable, or deteriorating.

For example:

- improving stability may justify less frequent reviews

- weakening signals may require tighter controls and closer follow-up

For quick reassessments, an online company credit report may be enough to decide whether to pause a limit increase, shorten terms, or apply additional safeguards.

Mini case: stopping a late-payment chain reaction

A packaging supplier sells to a regional food wholesaler on 45-day terms. After six clean months, the customer asks for:

- a 30% limit increase to support a new contract

- a move from 45-day terms to 60-day terms

Through weekly business monitoring, the supplier identifies two changes:

- the customer’s address and director details have recently changed

- new dispute signals appear in market feedback

Instead of rejecting the request entirely, the supplier restructures the exposure:

- approves only a 10% temporary limit increase for two billing cycles

- keeps payment terms at 45 days

- splits shipments into three smaller lots, releasing the next lot only after partial payment

Two months later, the wholesaler begins paying multiple suppliers late. The packaging supplier still gets paid with manageable delays because exposure was controlled before risk accelerated.

Practical checklist: a simple monitoring workflow

You do not need a complex system to make monitoring useful. A simple structure is often enough.

1) Segment your portfolio

Start with the customers that create the greatest downside if they weaken, such as the accounts with the highest open balance or longest terms.

2) Define triggers that require action

Examples include new disputes, status changes, repeated delays, or sudden requests for longer terms.

3) Set review frequency by exposure and risk

A simple approach could look like this:

- high exposure: weekly or biweekly

- medium exposure: monthly

- low exposure: quarterly, or before any change in terms or limit

4) Decide in advance what each trigger changes

If warning signals appear, decide whether that should lead to tighter terms, lower limits, staged deliveries, or partial upfront payment.

5) Document the rationale

A short written explanation helps keep your customer risk assessment consistent across the team and reduces subjective decisions.

Turning alerts into decisions

Monitoring only adds value when it leads to clear action. A simple rule-based approach often works best:

- stable signals: keep current terms and limit in place

- uncertainty or limited data: avoid increasing exposure and consider shortening terms temporarily

- deteriorating signals: reduce the limit, require safeguards, and run a fresh review

This keeps customer risk monitoring practical and commercially useful rather than bureaucratic.

FAQ

What is the difference between monitoring and a one-time report?

A one-time report provides a snapshot of risk at a specific moment. Credit monitoring is an ongoing process that helps you detect meaningful changes and respond before losses increase.

Do I need monitoring for every customer?

Not necessarily. Start with customers that create the greatest potential downside, such as larger balances, longer terms, strategic dependency, or rapidly growing exposure.

Conclusion

Credit monitoring and business monitoring help you stay ahead of changing risk, especially when payment terms are extended and exposure grows gradually. When combined with clear triggers, periodic reviews, and disciplined action, they allow you to identify customer risk earlier, reduce surprises, and protect working capital without slowing down trade. To see how continuous business monitoring can help you identify customer risk earlier and act with greater confidence, visit Creditovision. https://portal.creditovision.com/login