Company Credit Checks: When and Why They Are Critical

Company credit checks are critical whenever a business is about to extend trust, exposure, or commercial value to another company. That applies before offering trade credit, approving a new customer, increasing a limit, signing a larger contract, or relying on a supplier whose failure could disrupt operations. At each of these points, the real question is the same: is the company behind the opportunity financially reliable enough for the commitment being considered?

This is why a structured review matters. In B2B trade, losses rarely begin with a surprise. They usually begin with assumptions that were never tested properly. A timely company credit check helps businesses evaluate risk before it becomes late payment, bad debt, supply disruption, or a costly commercial mistake.

Why company credit checks matter

Many commercial decisions are made under pressure. Sales teams want to move quickly, procurement wants continuity, and finance teams are expected to support growth without taking unnecessary risk. In that environment, it is easy to approve exposure based on momentum rather than evidence.

That is where company credit checks become essential. They help businesses assess whether the confidence being offered is supported by payment behavior, financial strength, legal standing, and overall stability. In practical terms, they strengthen credit assessment and improve day-to-day risk management without forcing the business to slow down unnecessarily.

When a company credit check becomes critical

A review can add value at many stages of the commercial cycle, but some situations make it especially important.

Before onboarding a new customer

A new customer may look promising, but it also creates uncertainty. Before offering open terms or any form of customer credit, businesses need to understand whether the company appears capable of paying under the proposed conditions. A structured credit check helps prevent weak counterparties from entering the portfolio too easily.

Before extending trade credit

Whenever delivery happens before payment is collected, exposure begins immediately. That is why trade credit decisions should be supported by a realistic view of the counterparty’s profile. A review at this stage helps determine whether the proposed limit, payment period, and order value are reasonable.

Before increasing limits or offering longer terms

A company that was acceptable in the past may no longer justify the same level of exposure today. If a customer requests higher limits, longer payment terms, or larger recurring volumes, a fresh review becomes more important. This is often where a customer risk check helps businesses decide whether growing exposure still fits the underlying profile.

Before signing a larger or longer-term contract

Contracts define legal rights, but they do not guarantee performance or payment. Before entering a more significant agreement, businesses should evaluate whether the counterparty has the stability to support that commitment over time. This becomes critical when margins are tight, recovery would be difficult, or the relationship may become strategically important.

Before depending on a key supplier

Risk does not sit only on the receivables side. A weak supplier can create major operational problems if it fails during the relationship. In those cases, a supplier risk check helps businesses evaluate whether the vendor is financially stable enough to support continuity.

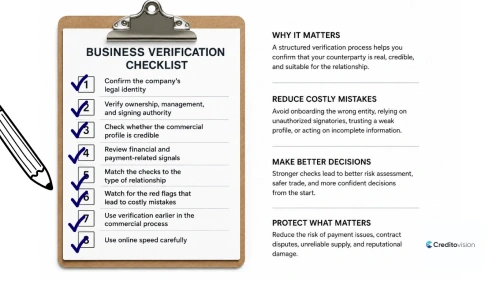

What a strong review should cover

A useful check should provide more than a simple yes-or-no answer. It should help businesses build a realistic view of the counterparty before exposure grows.

Identity and legal standing

The first step is to confirm that the company exists, is active, and is properly registered. This is where business verification matters. Businesses should know who they are dealing with, whether ownership is clear, and whether there are structural inconsistencies that deserve attention.

Payment behavior

Past payment discipline remains one of the clearest indicators of future reliability. If a company pays slowly, regularly stretches terms, or shows signs of weakening behavior, that should influence approval decisions. For many businesses, this remains one of the most practical parts of a customer risk check.

Financial strength

A company may appear active in the market and still be under financial pressure. Liquidity, profitability, and balance-sheet strength all matter when deciding whether the relationship is safe at the proposed level of exposure. This is one reason a company credit report is valuable: it helps explain not only whether risk exists, but also what may be driving it.

Legal and adverse signals

Court actions, enforcement activity, insolvency-related developments, or repeated structural changes can materially affect the quality of a relationship. A well-timed credit check should help surface these signs before approval, not after a problem begins.

Why timing is just as important as the check itself

One of the most common weaknesses in credit assessment is treating review as a one-time onboarding task. Risk changes over time. A company that looked stable during account opening may weaken later because of cash-flow pressure, market conditions, or internal disruption.

That is why timing matters. Reviews become especially important when:

- a new account is being opened,

- requested exposure increases,

- payment performance begins to slip,

- the contract becomes strategically important,

- or supplier dependency grows.

In supplier relationships, supplier risk monitoring can be just as important as the initial review. Ongoing visibility helps businesses detect deterioration before it affects continuity, delivery, or service quality.

How company credit checks support better decisions

The purpose of a review is not to reject every imperfect counterparty. The purpose is to match exposure to evidence. A moderate-risk company may still be acceptable under tighter terms, lower limits, shorter cycles, or closer review. A stronger company may justify more open terms because the underlying profile supports greater confidence.

Used properly, company credit checks help businesses:

- approve new relationships more carefully,

- set more realistic limits,

- reduce avoidable bad debt,

- strengthen alignment between sales and finance,

- and improve overall risk management across the portfolio.

For teams that need quick visibility during early screening, an online business credit report can also help identify which cases appear straightforward and which deserve deeper review before exposure is approved.

Why they are critical for growth as well as protection

Some businesses still view credit checks as purely defensive. In reality, they also support smarter growth. When decision-makers have a clearer view of counterparty strength, they can approve opportunities with more confidence, structure deals more intelligently, and expand with better control.

That is why these checks are critical not only for avoiding loss, but also for supporting sustainable growth. They help businesses say yes more intelligently, not simply say no more often.

Conclusion

Company credit checks are critical because they help businesses decide when trust is justified, when caution is necessary, and how much exposure a relationship can reasonably support. Whether the decision involves a new customer, extended trade credit, a major contract, or reliance on a key supplier, timely review can prevent costly mistakes before they become real losses. To support your credit assessment process with dependable credit reporting and company intelligence, visit the Creditovision portal: https://portal.creditovision.com/login