Business Credit Report: What It Is and Why It Matters Before Any Deal

A business credit report helps you determine whether a company is likely to make timely payments before signing a contract or granting trade credit. It provides a structured view of risk before signing a contract or extending terms, ensuring decisions are based on evidence, not assumptions.

Definition: What is a Business Credit Report?

A business credit report is a summary of a company's credit information, including its identity, payment behavior signals, legal status, and risk indicators, and is used for credit assessment and making more secure trade credit decisions.

What Does a Typical Business Credit Report Include?

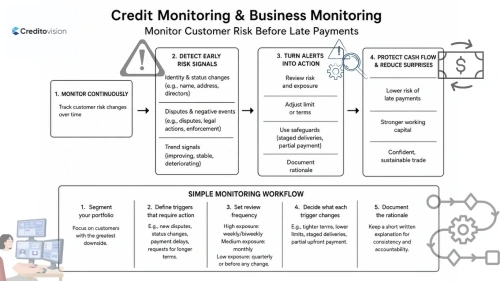

A well-prepared report focuses on areas critical to decision-making, such as:

• Company information: legal name, registration identifiers, status (active/passive), ownership and structure

• Payment behavior signals (if available): late payment patterns or stress indicators

• Legal and negative events: disputes, bankruptcy proceedings, insolvencies or other warnings that could affect solvency

• A risk indicator summarizing the overall risk level (typically a risk score)

These reports are typically compiled by credit rating agencies and used to support risk assessment.

Why It Matters Before Any Deal

1) Credit Check and Risk Assessment

A credit check can reveal early warning signs such as repeated late payments, sudden ownership changes, or legal disputes; signals that can easily be overlooked if you only examine a website or marketing materials.

2) It protects cash flow when extending trade credit

When you offer 30/60/90-day terms, you are effectively financing the customer. A business credit report helps you set safer terms, limits, and safeguards before exposure grows.

3) It supports KYC in business onboarding

During the business onboarding process, KYC (Know Your Customer) is not only compliance but also a fundamental safeguard against dealing with an improper legal entity or a risky counterparty.

4) Long-Term Stability

Reviewing a credit risk report before signing reduces the risk of default and helps build partnerships based on realistic expectations rather than optimistic forecasts.

Red Flags Worth Treating Seriously

Even one of these can justify tighter terms:

- The legal entity used in contracts doesn’t match invoices, emails, or the website brand

- Sudden changes in ownership/directors/address shortly before a large credit request

- Ongoing disputes or repeated negative events

- A high risk score paired with a request for long terms

Mini Case: A Safer Decision Before Signing

AN exporter receives an attractive order from an European distributor. The distributor looked legitimate—professional website, confident emails, and attractive purchase orders and pushes for 60-day terms.

Before signing, the exporter requests a business credit report. It shows elevated credit risk signals and recent disputes. Instead of rejecting the deal outright, the exporter proposes safer terms: partial prepayment and smaller, staged shipments. The distributor refuses—saving the exporter from a likely collection problem.

Practical Checklist: How to Use the Report

Use this quick workflow:

- Confirm company information matches the contracting party (name + identifiers + status).

- Scan for negative events and recent changes (ownership, directors, address).

- Compare the risk indicator to your planned exposure (order size, limit, term).

- Decide the control you need: shorter terms, staged delivery, partial upfront payment, or no open credit.

- Document the decision so future reviews are consistent (simple risk management discipline).

Example: Turning Risk Into Terms (Simple Rules)

- Lower risk: standard terms, standard limit

- Medium risk / limited data: smaller limit + shorter terms

- Higher risk: avoid open terms; use secured methods (advance payment, LC) or require stronger safeguards

This ensures that decisions are evidence-based without overcomplicating the process.

How often should I run a credit check?

For new partners, check before the initial agreement. For existing partners, check again before increasing limits, renewing contracts, or when there are changes in payment behavior.

What if financial statements are missing?

That’s common in many markets. Treat missing financials as “higher uncertainty” and mitigate with smaller limits, shorter terms, staged shipments, or secured payment methods.

A business credit report is more than just paperwork; it's practical assurance. Whether you're reviewing a company credit report for a local buyer or using international credit report information for cross-border trade, you gain clarity to make informed decisions. With the right credit reporting approach, you can protect cash flow, improve partner selection, meet KYC expectations, and reduce losses from preventable risks.

Explore Creditovision to see how trusted business credit reports can help you evaluate partners with greater confidence and reduce risk before any deal. https://portal.creditovision.com/login