International credit report: How to Prevent Costly Cross-Border Payment Surprises

An international credit report is one of the most effective tools for preventing costly payment surprises in cross-border trade. When companies sell on trade credit abroad, even small uncertainties—such as legal entity confusion, hidden disputes, or sudden operational instability—can quickly turn into delayed payments and expensive collection issues. A timely international credit check helps identify those risks before they affect cash flow.

Why cross-border payment surprises happen

International trade creates layers of uncertainty that are easier to underestimate at the start of a relationship.

Common causes include:

- Entity confusion: the company name used in emails or negotiations may not be the exact legal entity you can contract with or enforce against.

- Uneven transparency: the availability of public records, financial disclosure, and business data varies widely from one country to another.

- Slower enforcement: disputes, debt recovery, and legal follow-up often take longer across borders.

- Rapid structural change: ownership, management, or operating details can shift quickly, especially in stressed or volatile markets.

These issues often remain hidden during the first deal. The real problem usually appears later, once you have extended trade credit and exposure starts to grow.

What an international credit report helps you prevent

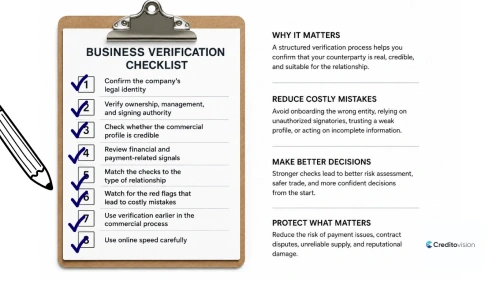

1) Contracting with the wrong entity

An international credit report supports business verification by confirming legal identity and core company information. This helps reduce invoice disputes, documentation errors, and cases where a seller ends up dealing with a company that is different from the one it expected to hold accountable.

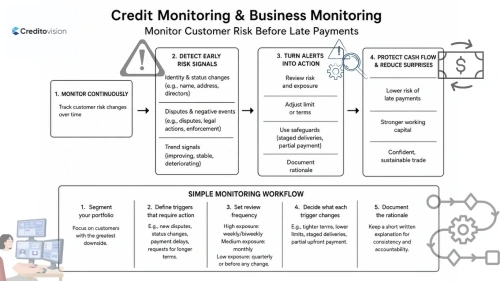

2) Exposure growing faster than your controls

When a new buyer asks for longer payment terms or a higher credit limit, the decision is no longer only about sales volume. It becomes a matter of credit assessment and risk management. A well-prepared report gives you structured credit information that supports more disciplined exposure decisions.

3) Hidden stress turning into late payment

Disputes, negative events, management changes, or unusual structural signals can all point to pressure before it becomes visible in your own receivables. This is where a proper risk assessment becomes valuable. Instead of reacting after a payment delay, you can identify warning signs earlier and adjust terms before the situation worsens.

4) Weak prospect selection in new markets

When entering a new country, companies often begin with target market analysis, build a marketing list, and identify potential customers. But not every prospect is suitable for open-account trade. Using an international credit report during the qualification stage helps you focus on businesses that are more likely to support stable, lower-risk growth. In broader expansion projects, a global company credit report can also help standardize early screening when you are comparing buyers across multiple countries.

Mini case: structuring a first order to avoid a loss

An exporter receives a first order worth €64,000 from a new buyer in Europe. The buyer requests 60-day terms and signals that a larger repeat order may follow next month.

Before approving the transaction, the exporter orders an international company credit report. The report shows recent management changes, dispute-related signals, and international company credit scores that indicate elevated risk.

Instead of rejecting the deal entirely, the exporter restructures the exposure:

- splits the order into two shipments

- sets terms at 30 days for the first two cycles

- requires 20% prepayment before the first shipment

- postpones any limit increase until two clean payment cycles are completed

The buyer accepts the revised structure. The exporter keeps the business opportunity while avoiding an uncontrolled first-deal exposure.

Practical checklist: how to use an international credit report to reduce surprises

- Confirm the exact legal entity before contracting.

- Review disputes, negative events, and recent changes first.

- Use score bands as guidance, then examine the reasons behind them.

- Translate the findings into clear terms, limits, and safeguards.

- Repeat the international credit check before increasing exposure or extending payment terms.

Conclusion

An international credit report helps prevent costly payment surprises by replacing assumptions with structured, decision-ready information. When combined with sound credit assessment and clear risk management practices, it allows companies to extend trade credit more confidently in international markets while keeping exposure under control. To learn how trusted international credit reporting can help you assess overseas partners more confidently, visit Creditovision. https://portal.creditovision.com/login